Financial Preparedness with Living Benefits

Most families do not get much support when life brings unexpected sickness or accidents. This quick survey helps identify blind spots and explore options before an emergency creates financial pressure.

Community Financial Preparedness Survey

Answer the questions below as accurately as possible. The goal is to help you think through income security, current protection, emergency cash, and practical next steps.

Why Financial Preparedness Matters

- In Ontario there are daily 1390 admissions and patients being treated in hallways due to sickness. Source provided: Google AI Mode link.

- Emergency Department visits are far more common than admissions. There were over 1.4 million injury-related emergency department visits in Ontario annually, meaning roughly 3,800 people visit an Ontario ER for an injury every day.

- Cancer Society reports approximately $33,000 is needed when a critical illness affects someone. A critical illness insurance plan can make a difference.

While most of us think, "It will never happen to me," critical conditions can touch anyone, anywhere, at any time, often without warning. Thanks to modern medicine, more people are surviving these events than ever before. However, you are likely to lose income during treatment and recovery, and in addition, your family may need help paying out-of-pocket medical expenses, plus everyday costs.

Cancer can affect anyone. Anywhere. Anytime.

Thanks to modern medical treatments, over 65% of Canadians diagnosed with cancer are expected to survive for five or more years after diagnosis. But diagnosis, treatment, and recovery can be expensive. Covering these unexpected costs, plus everyday expenses, can put a significant strain on your family's budget, especially if you lose income. The good news is a cancer insurance plan can make a difference.

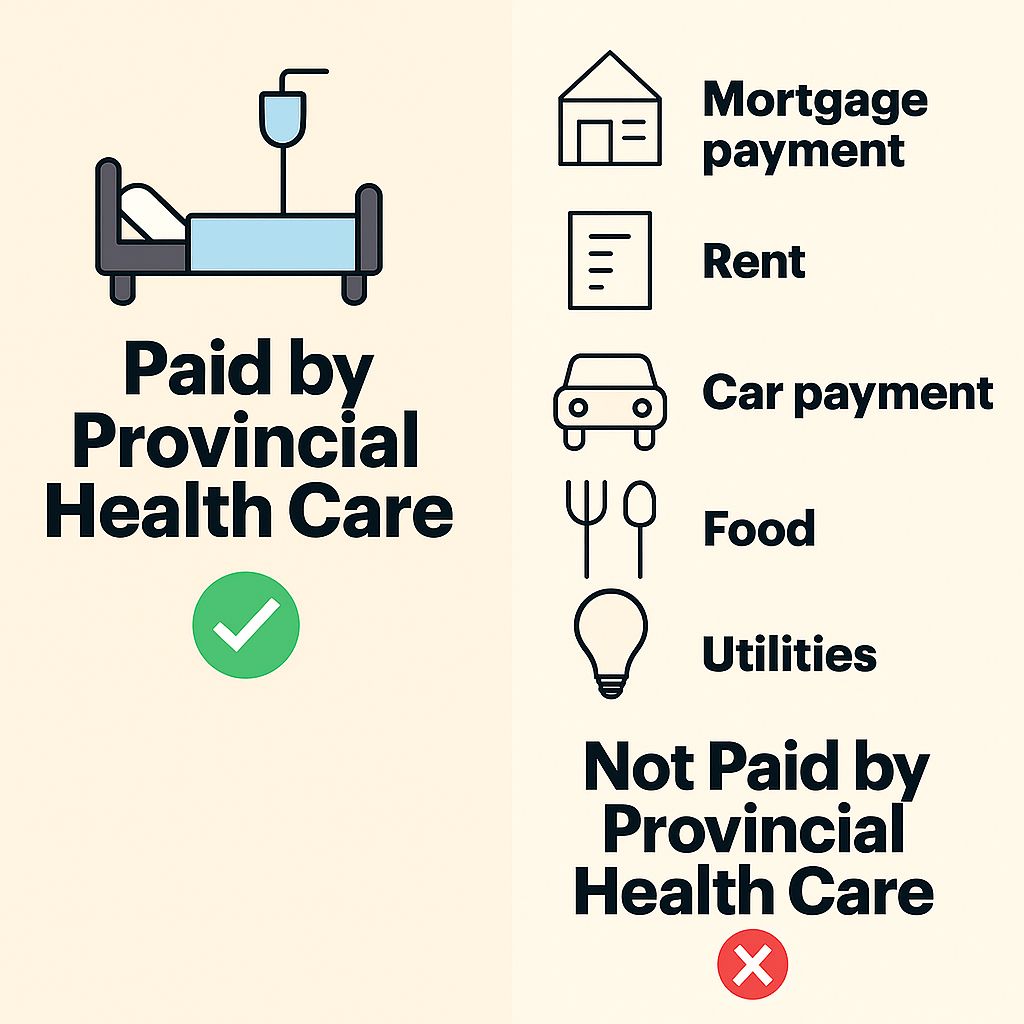

As an independent contractor, these plans are underwritten by Chubb, founded in 1882, and Combined, founded in 1922. Hardworking people are often not protected for regular bills and expenses when they get sick or injured, including mortgage, rent, food, gas, entertainment, childcare, phone, utilities, travel, business, taxes, and more. W. Clement Stone, founder of Combined and a peer of Napoleon Hill and Dale Carnegie, was nominated for the Nobel Prize. Learn more from the Napoleon Hill Foundation.

Warren Buffett's investment into Chubb confirms the strength of the company. These plans are underwritten by Combined since 1922 and owned by Chubb since 1882. Source provided: Warren Buffett and Chubb search.

There are two gaps that we fill

Cash for living expenses and wealth protection when sickness or accident hits, with 24/7 coverage in Canada and the USA.

Critical illness gaps for 35 conditions all the way until end of life for the whole family, including children, with return of premium when there is no claim.

Affordable and for everyone, including children and nonworking spouses. These plans are designed to provide peace of mind when you have coverage, support when you receive a diagnosis or injury, and value when there is no claim through return of premium. The core premise is simple: bills and expenses do not stop coming when someone is sick or injured.

Affordable and for everyone, including children and nonworking spouses. These plans are designed to provide peace of mind when you have coverage, support when you receive a diagnosis or injury, and value when there is no claim through return of premium. The core premise is simple: bills and expenses do not stop coming when someone is sick or injured.